- Alan Perkins received an £800 tax bill from HMRC because his total annual income from the State Pension and SERPS top-ups exceeded the UK’s frozen personal allowance of £12,570.

- Although he had no private pension, the legacy SERPS scheme pushed his income to around £16,500, making a portion taxable at 20%. This situation is becoming increasingly common for pensioners across the UK.

- Key Points:

- State Pension is taxable income when it exceeds the allowance

- SERPS top-ups contributed to Alan’s tax liability

- Personal allowance freeze until 2031 increases fiscal drag

- New exemption policy excludes SERPS pensioners

- Experts warn of a growing tax burden on retirees

- Real-life cases show widespread confusion and unfairness

-

What Exactly Happened To Alan Perkins And Why Was He Taxed £800?

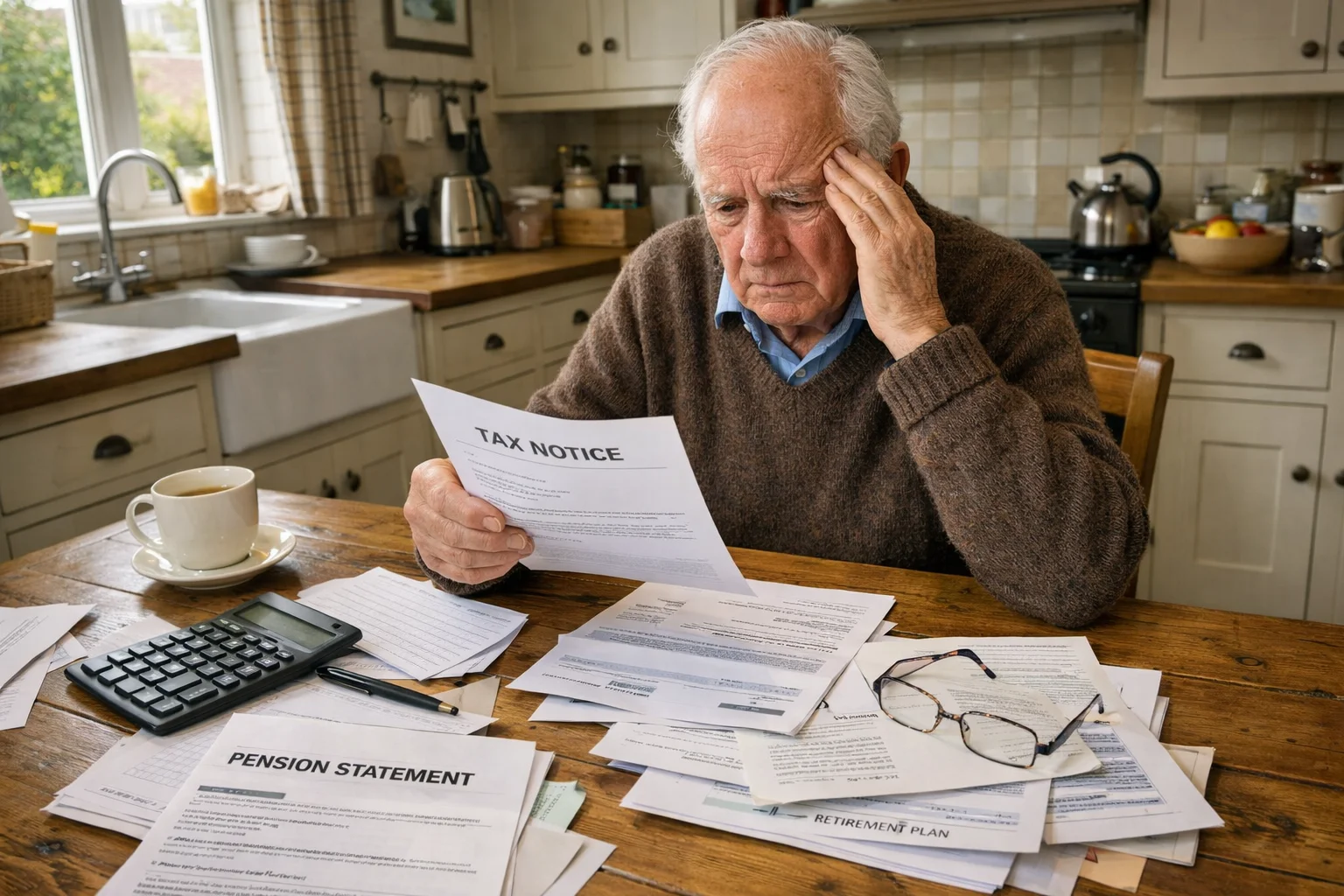

- Alan Perkins is a 71-year-old retired heating engineer who believed that his decades of work would earn him a tax-free State Pension.

- After leaving school at 15, he worked long shifts, often from early morning until late at night, and even worked weekends as a minicab driver to support his family.

- Like many who contributed consistently to National Insurance, Alan assumed retirement would be financially straightforward.

- But in early 2025, he was issued a tax bill from HMRC for £800. This caught him off guard.

- Alan’s total income came from his State Pension and historical top-ups from the State Earnings-Related Pension Scheme (SERPS), totalling around £16,500 annually.

- The crux of the issue is that this figure exceeds the personal tax-free allowance, which has been frozen at £12,570 since 2021. As a result, the remaining £3,930 was taxed at 20 percent, resulting in a charge of around £800.

- Alan’s case is not isolated. Thousands of pensioners with modest enhancements to their pension income are falling into similar traps, often without warning.

-

Key Takeaways From Alan’s Case

- Income from the State Pension and SERPS combined exceeded the personal allowance

- HMRC issued a tax bill as the excess income became taxable at 20 percent

- Many pensioners believe the State Pension is tax-free and are unaware of income tax thresholds

- Historical earnings-based schemes like SERPS are no longer active but still influence pension totals

-

Why Is The State Pension Being Taxed In The First Place?

- The UK State Pension is classified as taxable income, though tax is not deducted at source. This creates confusion for many pensioners who receive only State Pension income and are not used to interacting with HMRC.

- Unlike salaries or occupational pensions, the State Pension does not operate under Pay As You Earn (PAYE). If a person has no other income, tax may not be collected immediately. However, if their income from the State Pension alone or in combination with other pensions surpasses the personal allowance, a tax bill can follow.

- For Alan Perkins, the tipping point was the additional payments from SERPS, which put his total income over the limit. Because of the way HMRC calculates income and applies codes, these payments often go unnoticed until a bill is issued.

-

Summary Of Tax Application On Pension Income

-

Source Of Income Tax Deducted At Source Taxable Above £12,570 Automatically Reported Basic State Pension No Yes No SERPS No Yes No Private Occupational Pension Yes (PAYE) Yes Yes Deferred Pension Lump Sum No Yes No

- The tax treatment differs based on the source, which is where much of the misunderstanding arises.

-

What Role Did SERPS And Historical Top-Ups Play In Alan’s Tax Bill?

- SERPS was introduced in 1978 to reward employees with a higher earnings history by topping up their basic State Pension. The idea was to offer a more generous retirement to workers who paid more in National Insurance.

- Although the scheme ended in 2002, those who contributed during its operation still receive the benefits.

- Alan was one of those contributors. His years of overtime and regular work boosted his contributions and, by extension, his SERPS entitlement.

- While this initially seemed like a reward, it now functions more like a liability.

- SERPS increases are counted toward taxable income, despite being state-managed. For many, this means their pensions now breach the tax-free threshold, even without private pensions.

-

Income Breakdown Example: Alan Perkins

-

Income Source Annual Amount Tax Status Basic State Pension £11,973 Non-taxable SERPS Top-Up £4,527 Taxable Total Pension Income £16,500 £3,930 taxable Tax Rate Applied 20% £800 bill issued

- Alan’s case demonstrates how small additions from legacy schemes can trigger significant tax implications.

-

How Does The Personal Allowance Freeze Impact Pensioners?

- Since 2021, the personal tax-free allowance has been frozen at £12,570. While inflation and the triple lock have increased pension incomes, the tax-free threshold has not risen accordingly. This mismatch leads to what is known as fiscal drag, where more people are drawn into paying tax simply due to static thresholds.

- The government’s decision to freeze the personal allowance until 2031 further compounds the issue. Each year, the State Pension rises, potentially bringing more pensioners into taxable territory.

-

Effect Of Allowance Freeze Over Time

-

Tax Year Personal Allowance New State Pension Excess Income Tax Due (Approx) 2023 £12,570 £10,600 £0 £0 2025 £12,570 £12,547 £0 £0 2027 £12,570 £13,400* £830 £166 2031 £12,570 £14,700* £2,130 £426

- *Estimated based on triple lock projections

- Alan’s situation today could become the norm by 2027 if no adjustments are made to the personal allowance.

-

Who Will Benefit From Rachel Reeves’ New Pension Tax Exemption Policy?

- Chancellor Rachel Reeves has introduced a targeted exemption for pensioners whose only income is the basic or new State Pension, with no other enhancements.

- This policy aims to prevent low-income pensioners from receiving minor tax bills that are costly for HMRC to administer.

- However, this exemption excludes pensioners like Alan whose pension income is increased through schemes like SERPS, even though these are not private earnings.

- The policy, though well-intentioned, creates a two-tier system where those with nearly identical incomes face different tax treatments based on how their pensions are structured.

-

Comparison Of Who Qualifies For The Exemption

-

Pensioner Type Income Source Qualifies For Exemption? Basic State Pension Only £11,973 Yes New State Pension Only £12,547 Yes State Pension + SERPS (like Alan) £16,500 No State + Private Pension £20,000+ No

- This exclusion leaves many pensioners feeling ignored by the new policy.

-

Why Are Experts Criticising The Current Pension Tax Policies?

- As someone who has followed UK tax policy closely, I’ve seen increasing pushback from former ministers, economists and pension experts over the handling of pensioner tax.

- The growing reliance on legacy schemes like SERPS, combined with frozen allowances, has made the system inconsistent.

- Two people with nearly identical financial situations may face completely different tax liabilities.

- Experts have labelled this a “cliff-edge” policy where falling just outside the exemption threshold leads to disproportionate consequences.

- Former Pensions Minister Sir Steve Webb has described the policy as “completely indefensible.” Baroness Ros Altmann also warned that “people on the wrong side of the cliff-edge will be unfairly penalised.”

- Having spoken to pensioners who received unexpected tax bills, the sentiment is often one of betrayal. They contributed for decades and expected the State to reward, not penalise, them in retirement.

-

Expert Reactions On The Policy

-

Expert Name Title/Position Key Comment Sir Steve Webb Former Pensions Minister “Completely indefensible” Baroness Ros Altmann Former Pensions Minister “Policy is fraught with risk” Low Income Tax Reform Group Policy Think Tank “Adds complexity and risks being unfair”

- This discontent is spreading, particularly among pensioners who don’t understand why their neighbours qualify for exemptions while they are being taxed.

-

How Could This Issue Affect More Pensioners In The Coming Years?

- As the triple lock continues to lift the State Pension while the personal allowance remains unchanged, more and more pensioners will find themselves being taxed. This slow but steady process, known as fiscal drag, is especially difficult for pensioners with no other income or assets.

- For people in Alan’s position, it means a future where their tax bills steadily rise despite no real increase in living standards. According to Treasury projections and independent think tanks, the number of pensioners paying income tax could rise from 8 million in 2024 to nearly 10 million by 2027.

-

Estimated Growth Of Pensioners In Tax Scope

-

Year Pensioners Paying Tax Primary Cause 2023 7.9 million Triple lock rise + frozen threshold 2025 8.7 million No change in allowance 2027 9.8 million (projected) Continued fiscal drag 2031 10.5 million (estimate) Long-term allowance freeze

-

A Real-Time Example: Margaret From Kent

- Margaret Taylor, a 69-year-old former administrative assistant from Kent, recently shared her experience on a consumer advice forum. Having never contributed to a private pension, Margaret relied solely on the new State Pension and a minor SERPS enhancement of around £2,800 per year.

- Her total pension income in 2025 reached just over £15,300, putting her £2,730 above the personal allowance threshold. Like Alan Perkins, she was unaware that this modest increase would trigger a tax bill. A few months after her retirement, she received a letter from HMRC stating that she owed £546 in unpaid tax.

- Speaking to a local newspaper, she said:

- “I always thought my pension would be tax-free. I live alone, manage every pound carefully, and I don’t have any other income. I had no idea SERPS would count like this. Getting that bill felt like being penalised for working hard.”

- Margaret has since applied for Marriage Allowance in retrospect and sought guidance from Citizens Advice, but she remains frustrated that such a small increase resulted in a bill she wasn’t prepared for.

- This example illustrates just how easily pensioners with low or moderate incomes can fall into the tax net, especially when adjustments like SERPS are involved.

- Margaret’s situation, much like Alan Perkins’, reinforces the need for clearer communication from HMRC and more equitable tax policy frameworks.

-

What Can Pensioners Do To Reduce Or Avoid Pension Tax Shocks?

- While pensioners have limited control over government tax policy, there are several strategies they can use to manage or reduce their liability.

- Review your HMRC tax code regularly to ensure it reflects accurate income sources

- Consider using the Marriage Allowance if your spouse earns below the personal allowance

- Keep detailed records of pension sources to avoid confusion with HMRC

- Engage a financial adviser if your pension income is close to or above the threshold

- Monitor annual pension increases to anticipate future tax bills

- These steps, though small, can help pensioners stay informed and proactive.

-

Conclusion

- Alan Perkins’ £800 tax bill is not an isolated case. It’s a warning sign of systemic issues within the UK pension and tax framework.

- The freezing of the personal allowance, the complexity of legacy schemes like SERPS, and poorly targeted exemptions all point to a growing burden on pensioners who had little expectation of being taxed in retirement.

- The policy changes introduced by Rachel Reeves aim to address some of the administrative burden but fall short of creating fairness. Thousands of pensioners, like Alan, may continue to face growing tax bills despite relying solely on the State Pension.

- If the government does not rethink the broader structure, more pensioners will face similar shocks undermining confidence in a retirement system that was meant to offer security and dignity.

-

FAQs

-

What is SERPS and how does it affect my State Pension?

- SERPS (State Earnings-Related Pension Scheme) was a top-up scheme from 1978 to 2002. It adds to your pension income but can push you above the tax threshold.

-

How can I check if my State Pension is taxable?

- Add up all pension income and compare it to your personal allowance. If it’s over £12,570, the excess is taxable.

-

Will Rachel Reeves’ pension tax exemption apply to me?

- Only if your sole income is the new or basic State Pension, without SERPS or private pensions.

-

What happens if I’ve underpaid tax on my pension?

- HMRC will typically issue a tax bill or adjust your tax code to recover the amount in future years.

-

Is there a way to avoid tax on my pension?

- Not entirely, but you can reduce your liability by using tax allowances like the Marriage Allowance.

-

Why is the personal allowance frozen until 2031?

- It’s a government fiscal strategy to increase tax revenue without changing tax rates a form of fiscal drag.

-

Can I appeal a pension tax bill from HMRC?

- Yes, if you believe there’s been a mistake. Contact HMRC or a tax adviser for help.

Leave a Reply